Click & Buy: The Digital Race Fueling Fashion Overconsumption

The frenzy of modern fashion now plays out online, a stage for unprecedented competition. Numerous players jostle for attention, from own brand retailers to specialised or generalist platforms and secondhand marketplaces. All compete in a digital ecosystem where the race to catch the latest trends fuels relentless consumerism.

The online ecosystem, accelerating the sector’s growth

By 2025, 25.7% of the total European and UK fashion market was already generated online, amounting to around €131.4 billion, according to the latest Cross-Border Commerce Europe report. While several brick-and-mortar retailers have built a strong online presence (Zara, H&M, Uniqlo, Mango, C&A and others), it is above all the multi-brand online platforms that are experiencing the most rapid growth, capturing the overwhelming majority of online fashion purchases (around 82% of the e-commerce apparel market). European pure players such as Zalando, ASOS, Spartoo and Next, now competing alongside international specialist platforms like Shein and generalist marketplaces including Temu, Wish, AliExpress and Amazon, are battling for market shares. By mid-2025, Shein alone had reportedly reached 145.7 million monthly unique users across the continent.

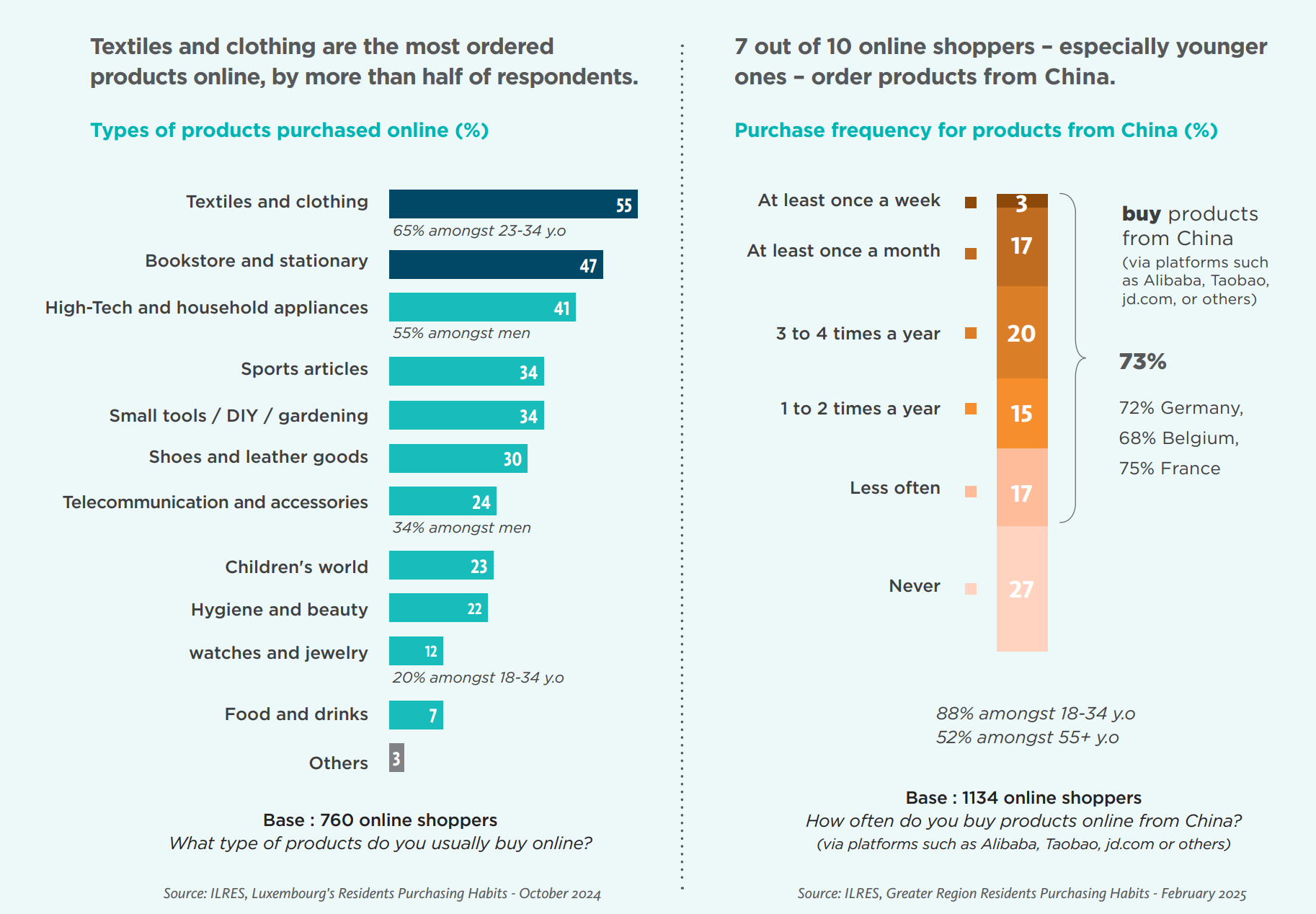

Fashion is in fact what people buy most online. It stands as the leading segment of digital commerce in Europe, with 70% of online shoppers buying clothing, footwear or accessories, according to Ecommerce Europe’s 2025 report. Luxembourg is no exception. Clothing is the most frequently purchased category online, with 55% of residents surveyed saying they buy fashion items on the web, according to a 2024 TNS Ilres study. The habit is particularly entrenched among younger consumers, reaching 65% among those aged 25–34. A 2025 survey by the same institute across the Greater Region shows that 73% of online shoppers make purchases on Chinese platforms (rising to 88% among 25–34-year-olds), across all product categories.

Driving More Compulsive Buying

In this digital race, platforms aim above all to encourage impulse purchases by constantly simplifying the buying process: this is the Click & Buy strategy. The goal? To reduce the number of abandoned carts, as many users fail to complete their orders. The figure is remarkably high: 76% according to a 2025 study by SellersCommerce. The approach consists in removing as many steps as possible between desire and purchase by minimising typical frictions (account creation, entering payment details, providing an address, confirming the order and so on), pre-filling and automating these steps, and making the interface ever more seamless.

This strategy is reinforced by fast delivery and easy returns. Together, these mechanisms contribute to the trivialisation of the act of purchasing. The ideal outcome? Being able to buy, in one click, a flash-sale item spotted on TikTok or Instagram.

Inside the Ultra-Fast Culture

This acceleration-driven logic of shopping is largely fuelled by strategies that rely heavily on social media. Far from the traditional four seasonal fashion cycles aligned with the calendar seasons, micro-trends now succeed each other sometimes every 24 to 48 hours on TikTok and Instagram. The real-time scrolling of trends aims to maximise immediacy. As soon as a look goes viral, players like Shein and Temu produce cheap copies as quickly as possible in order to keep pace with this programmed obsolescence, raising questions about intellectual property, environmental issues, and social compliance.

Social media has long surpassed its role as a mere communication channel, becoming an active driver of the ultra-fast culture. The constant staging of consumerism by highly influential influencers pushes the normalisation of frequent, low-cost purchases. They showcase themselves through hauls, in other words videos displaying large quantities of items bought at once, often from a single retailer. Another popular format is the unboxing video, which films the moment a parcel is opened. Influencers also enjoy showing their outfit of the day (OOTD), which, naturally, is expected to change daily.

However, these posts are no longer exclusive to professional content creators; ordinary consumers are increasingly taking part, amplifying trends and acting as free advertising channels for brands. Appearance has become so central on social media that posting two outings in the same outfit is sometimes socially perceived as awkward. Hyper-consumerism tends to become a social norm.

Credit : Revolve

AI and the Next Leap in the Great Acceleration

All stages of the fashion process are being accelerated with the emergence of AI in the industry. Design comes first, with the possibility of assisting creative phases through AI by providing simple prompts or inspirational images. AI enables the industry to respond more closely to consumer expectations. Google and Zalando’s Muze project is precisely aimed at leveraging code to integrate potential customers’ preferences in record time, resulting in 40,424 designs generated within the first month. Moreover, AI claims to anticipate trends. For example, Heuritech analyses over three million images circulating on social media every day, from celebrities to ordinary users, to predict the looks that will become popular.

Production is also optimised through algorithms, from supply chain management to quality control and automated fabric cutting. Promotion of items is carried out in the blink of an eye, with AI generating advertising content and editorial copy. Revolve, which made waves with its 100% AI-driven campaign, has taken a further step by launching its AI-assisted customer experience with CoPilot. Brands are now developing so-called intelligent shopping assistants capable of advising customers via a conversational interface, without the need to browse the entire catalogue. This is the case with Ssense, the Canadian online luxury retailer, which has integrated an OpenAI-powered chatbot to provide personalised style recommendations. ChatGPT’s Luxury Personal Shopper also targets this market. The ultimate goal remains the same: to trigger purchases faster and in ever greater numbers.

The Myth of Online Second-Hand Shopping

Buying second-hand is widely seen as a responsible way to dress, extending the life of garments without driving new production. However, while this is arguably true for "slow" purchases made in small boutiques, the digital era has completely transformed the concept. Platforms such as Vinted, Depop, ThredUp, Wallapop, and Vestiaire Collective have thrived. Yet the promises of more sustainable fashion through a widespread online second-hand market face a stark ecological reality. A 2025 study by the French agency Ademe highlights the pitfalls of these resale platforms. "Analysis of consumption volumes among users confirms a highly consumerist logic.

Second-hand platform users are often among the biggest clothing consumers, despite having a slightly below-average clothing budget." Among their motivations, the main drivers are finding "good deals" and buying more clothing, rather than frugality or sustainability. A rebound effect is observed in 51% of cases, where savings are spent on new purchases, creating a consumerist spiral. The result: purchases are often of lower quality (38% of users consume fast-fashion second-hand items), many orders end up regretted and unused in wardrobes forming the so-called "idle stock", and ultimately, resold items rarely experience a full first life; the items resold have typically lived only 19 to 30% of a normal garment lifespan.

These digital second-hand players, which once promised the advent of responsible fashion, in reality encourage the multiplication of transactions and have become incredible platforms of hyper-consumption. Whether second-hand or new, fashion today seems excessively immediate… just a click away.